Loans Zimbabwe: Your Guide to Navigating the Lending Landscape

Accessing loans in Zimbabwe can be crucial for personal and business growth. Understanding the various loan options, requirements, and the current lending climate can empower you to make informed financial decisions. This guide will explore the intricacies of loans in Zimbabwe, helping you navigate the process effectively.

Different types of loans cater to various needs. Personal loans can help with unexpected expenses or consolidate debt, while business loans can fuel expansion and growth. Understanding the specifics of each loan type is essential. What are the interest rates? What are the repayment terms? These questions are paramount when considering a loan.

Types of Loans in Zimbabwe

Navigating the loan landscape begins with understanding the diverse types of loans available. From short-term emergency loans to long-term mortgages, each loan product has its own set of characteristics. Let’s delve into some common types:

Personal Loans

Personal loans offer a flexible way to access funds for various personal needs. These loans are typically unsecured, meaning you don’t need collateral to qualify. However, this often translates to higher interest rates.

What are the eligibility criteria for personal loans in Zimbabwe? Typically, lenders consider your credit score, employment history, and income level. Having a strong credit history increases your chances of securing a loan with favorable terms.

Business Loans

For entrepreneurs and business owners, securing a business loan can be instrumental in achieving growth objectives. These loans can finance expansion projects, purchase equipment, or manage working capital.

Business loans may be secured or unsecured, depending on the lender and the loan amount. Lenders often require a detailed business plan and financial projections to assess the viability of the business.

Home Loans (Mortgages)

Owning a home is a significant milestone, and home loans make this dream attainable for many. Mortgages are long-term loans secured by the property itself.

Interest rates for home loans can be fixed or variable, impacting your monthly repayments. Understanding the intricacies of mortgage agreements is essential before committing to such a long-term financial obligation.

Understanding Loan Requirements in Zimbabwe

Before applying for a loan, it’s essential to understand the requirements. While these vary depending on the lender and loan type, some common requirements include:

- Proof of Identity: A valid national ID or passport is typically required.

- Proof of Residence: This can be a utility bill or a bank statement showing your current address.

- Proof of Income: Payslips or bank statements demonstrating your ability to repay the loan.

- Credit Report: Lenders may review your credit history to assess your creditworthiness.

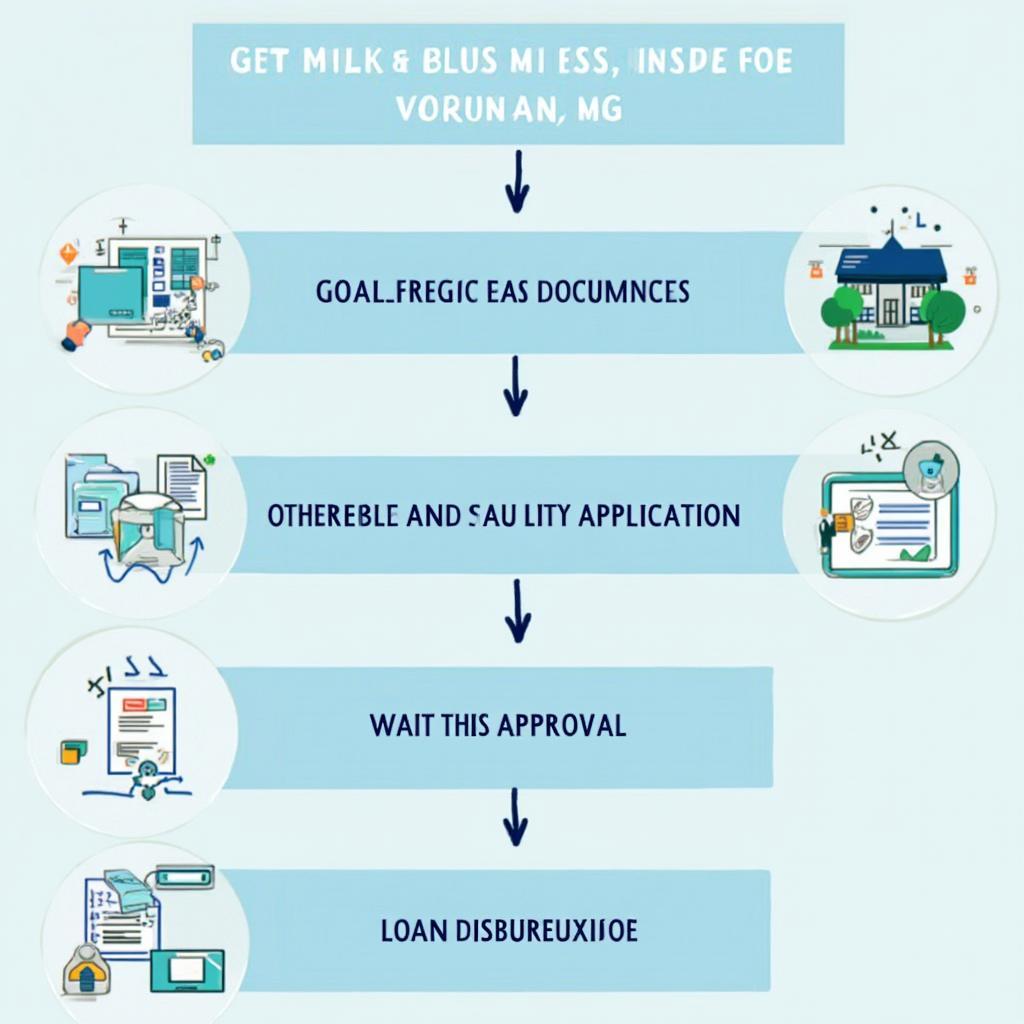

Navigating the Loan Application Process

The loan application process can seem daunting, but understanding the steps involved can simplify it. Generally, the process involves:

- Research and Compare: Explore different lenders and loan products to find the best fit for your needs.

- Gather Documents: Prepare all necessary documents, such as proof of identity, residence, and income.

- Complete the Application: Fill out the loan application form accurately and completely.

- Submit Application: Submit your application and supporting documents to the lender.

- Await Approval: The lender will review your application and notify you of their decision.

“Thorough research is paramount before committing to a loan. Compare interest rates, repayment terms, and fees from different lenders to find the most favorable option,” advises Tapiwa Muchenje, a Senior Financial Advisor at a leading Zimbabwean bank.

Risks and Considerations

While loans can be beneficial, it’s crucial to understand the associated risks:

- High Interest Rates: Some loans, especially unsecured loans, can carry high interest rates.

- Debt Trap: Borrowing more than you can afford can lead to a cycle of debt.

- Impact on Credit Score: Defaulting on loan repayments can negatively impact your credit score.

Loan Application Process in Zimbabwe

“Always borrow responsibly. Ensure you have a clear repayment plan and understand the implications of defaulting on your loan,” cautions Rudo Moyo, a Financial Literacy Advocate based in Harare.

usd loans in zimbabwe contact details

Conclusion

Navigating the loans landscape in Zimbabwe requires careful consideration and understanding. By researching different loan options, understanding the requirements, and considering the potential risks, you can make informed decisions that align with your financial goals. Remember to borrow responsibly and create a sustainable repayment plan. Begin your journey towards securing the right loan for your needs today.

FAQ

- What is the average interest rate for personal loans in Zimbabwe? Interest rates vary depending on the lender and your creditworthiness.

- How can I improve my chances of getting a loan approved? Maintaining a good credit score and providing accurate documentation can improve your chances.

- What are the consequences of defaulting on a loan? Defaulting can negatively impact your credit score and may lead to legal action.

- Where can I find reputable lenders in Zimbabwe? Research online and consult with financial advisors for recommendations.

- What is the maximum loan amount I can borrow? Loan amounts vary depending on the lender and the type of loan.

- Are there any government-backed loan programs in Zimbabwe? Research government initiatives and programs that may offer loan assistance.

- How can I compare different loan offers? Use online comparison tools and consider factors like interest rates, fees, and repayment terms.