What is an MSHDA Loan?

MSHDA loans are Michigan State Housing Development Authority mortgages designed to make homeownership more accessible for Michigan residents. They offer various programs with features like down payment assistance, competitive interest rates, and rehabilitation options, catering to first-time homebuyers and those with moderate incomes.

Understanding the MSHDA Loan Program

The MSHDA loan program aims to provide affordable housing options to Michigan residents. It offers several different loan products, each tailored to specific needs and income levels. Whether you’re a first-time homebuyer navigating the market or looking to renovate your current home, MSHDA might have a solution for you. These loans can make a significant difference, helping people achieve their dream of owning a home in Michigan.

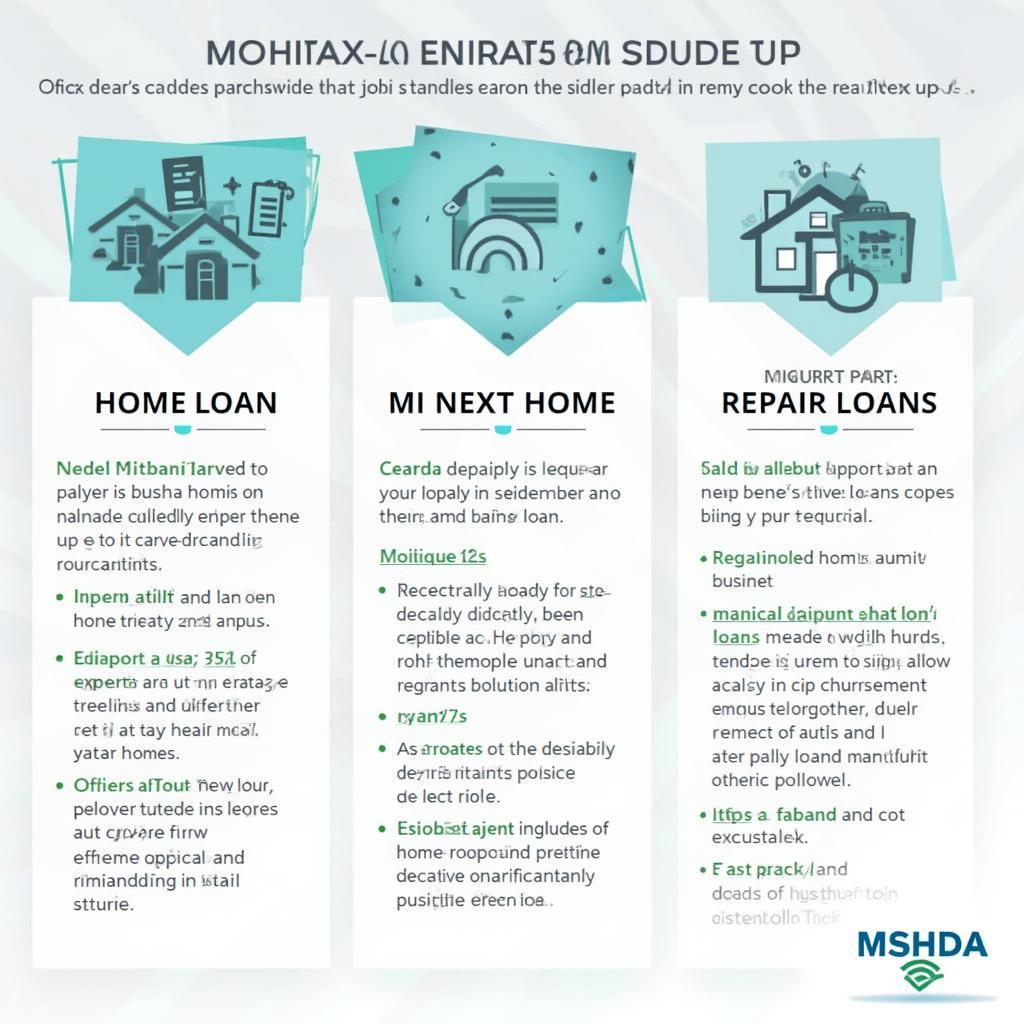

Types of MSHDA Loans

MSHDA offers a variety of loan programs, including:

- MI Home Loan: This program provides fixed-rate mortgages with down payment assistance for first-time and repeat homebuyers.

- MI Next Home: Designed for move-up buyers, offering competitive fixed interest rates.

- MSHDA Down Payment Assistance (DPA): This can be combined with other MSHDA loan products to assist with down payment and closing costs.

- Home Repair Loans: Offer financing for essential home repairs and improvements.

MSHDA Loan Types Explained

Who Qualifies for an MSHDA Loan?

Eligibility requirements vary depending on the specific MSHDA loan program. Generally, factors such as income limits, credit score requirements, and property location play a role in determining qualification. Potential borrowers must meet specific income and credit score guidelines. The property must also be located within Michigan.

Income Limits for MSHDA Loans

Income limits are based on household size and county of residence. These limits ensure that the programs benefit those who need them most. You can find the current income limits on the MSHDA website.

Understanding MSHDA Income Limits

Understanding MSHDA Income Limits

Credit Score Requirements for MSHDA Loans

While MSHDA loans aim to be accessible, there are still credit score requirements that applicants must meet. A good credit history demonstrates financial responsibility and increases the likelihood of loan approval.

Benefits of Choosing an MSHDA Loan

MSHDA loans offer several advantages, including:

- Low Down Payment Options: Many MSHDA programs require lower down payments than conventional loans.

- Competitive Interest Rates: MSHDA offers competitive interest rates, which can translate to significant savings over the life of the loan.

- Down Payment Assistance: Grants and forgivable loans may be available to assist with down payment and closing costs.

Applying for an MSHDA Loan

The application process involves completing the necessary paperwork, providing documentation, and working with a participating lender. It’s crucial to gather all required documents and work closely with your lender throughout the process.

Finding a Participating MSHDA Lender

MSHDA works with a network of approved lenders. You can find a list of participating lenders on the MSHDA website. Working with an approved lender streamlines the application process.

MSHDA Loan vs. Conventional Loan

MSHDA loans offer advantages for those who qualify, including lower down payments and potential down payment assistance. However, conventional loans may offer more flexibility in terms of property types and loan amounts.

Comparing MSHDA and Conventional Loans

Comparing MSHDA and Conventional Loans

“MSHDA loans are a valuable resource for Michigan residents seeking affordable homeownership. Understanding the different program options and eligibility requirements is crucial for a smooth and successful home buying experience,” says Nguyen Thi Lan Huong, Senior Mortgage Advisor at ABC Financial Group.

Conclusion

MSHDA loans offer a pathway to homeownership for many Michigan residents. With various programs catering to different needs, understanding the specifics of each MSHDA loan can help you make an informed decision and achieve your housing goals. Explore the MSHDA website and connect with a participating lender to learn more about how an MSHDA loan can benefit you.

“The down payment assistance offered by MSHDA can be a game-changer for first-time homebuyers,” adds Tran Van Minh, Financial Consultant at XYZ Finance. “It can significantly reduce the financial hurdle of entering the housing market.”

FAQ

- What is the maximum income limit for MSHDA loans? Income limits vary by county and household size. Check the MSHDA website for specific details.

- Do I need to be a first-time homebuyer to qualify for an MSHDA loan? Not necessarily. Some MSHDA programs are available to repeat homebuyers as well.

- What type of properties are eligible for MSHDA financing? Generally, single-family homes, condominiums, and townhouses are eligible.

- How do I find a participating MSHDA lender? You can find a list of approved lenders on the MSHDA website.

- Can I use an MSHDA loan for a vacation home? No, MSHDA loans are intended for primary residences.

- What is the typical interest rate for an MSHDA loan? Interest rates are competitive and can vary based on market conditions and the specific loan program.

- How much down payment assistance can I receive through MSHDA? The amount of down payment assistance varies depending on the program and your individual circumstances.

“Don’t hesitate to reach out to a housing counselor or a participating lender to discuss your individual financial situation and explore the best MSHDA loan option for you,” concludes Le Hoang Anh Tuan, Certified Financial Planner at DEF Financial Services.